Michigan Public Service Commission continues method of setting utility revenues based on projected future costs

Author

Stephen A. Campbell

On July 10, the Michigan Public Service Commission (“Commission”) issued an order in Case No. U-21637 (“Order”) reaffirming its approach to establishing Michigan utility revenues based on utilities’ projected future costs. It did so despite comments from numerous parties across myriad sectors including, among others, the Attorney General, Natural Resources Defense Council, Ecology Center, Michigan Environmental Council, Michigan Environmental Justice Coalition, Michigan League of Conservation Voters, Sierra Club, Association of Businesses Advocating Tariff Equity, and the Michigan Office of Administrative Hearings and Rules, explaining how this approach routinely results in utilities collecting tens of millions of dollars in rate revenue that is not needed to cover the cost of providing customers service.

Under MCL 460.6a(1), when a Michigan utility requests a revenue increase, it may use projected future costs and revenues for a future consecutive 12-month period in developing its requested rates and charges. If it does so, it must support its projections with competent, material, and substantial evidence. In practice, however, this process inherently places customers at a distinct disadvantage in interpreting and evaluating cost projections relative to the utilities. As the Commission recognized in its order requesting comments on this topic, “over the last seven years (while processing these cases within a compressed timeframe) the cases themselves have undergone an extraordinary expansion in size,” which “trend of expanding case record volume is reflected in virtually every rate case filed since 2016 and has clearly put a strain on the resources of all of the parties involved in these cases, including the Commission and its Staff.”

Thus, while in theory the utility has the burden to demonstrate the reasonableness of its future cost projections, in practice this burden only effectively applies when a projection (of which there are hundreds, if not thousands, in each rate case) is challenged. Furthermore, the practical burden of showing a projection’s shortcomings then effectively shifts to the challenging party, even if it is simply explaining the evidentiary shortcomings of the utility’s cost projection.

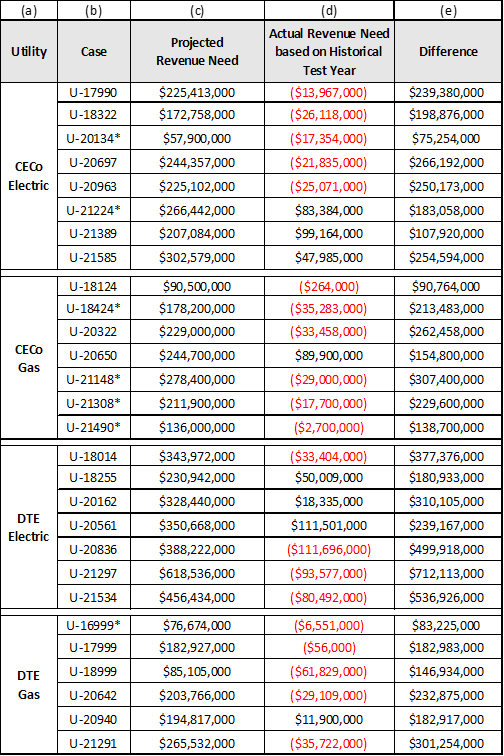

Establishing utility rates based on projections of future potential costs the utility has not yet incurred has resulted in Michigan’s largest utilities collecting tens of millions of dollars in rate revenue beyond that required to meet their costs to provide service:

Establishing utility revenues using projected potential future costs, therefore, consistently results in rates that collect more than the utility requires to meet its actual costs. Without utilizing an alternative approach to cost recovery, such as basing utility revenues on the historic costs it has actually incurred, adjusted for only truly known and measurable changes, Michigan utility customers will continue to face excessive rates that overcompensate the utilities and exceed the utilities’ cost to serve.

For further information or assistance regarding issues related to the Michigan Public Service Commission or energy law more generally, contact Stephen A. Campbell.

This publication is intended for general informational purposes only and does not constitute legal advice or a solicitation to provide legal services. The information in this publication is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. Readers should not act upon this information without seeking professional legal counsel. The views and opinions expressed herein represent those of the individual author only and are not necessarily the views of Clark Hill PLC. Although we attempt to ensure that postings on our website are complete, accurate, and up to date, we assume no responsibility for their completeness, accuracy, or timeliness.

Subscribe for the latest

Subscribe